The Mirage of "Free Money": A Story of Cross-Exchange Arbitrage

Why "free" arbitrage often isn't: contract mismatches, invisible costs, and execution risk.

You're scanning markets on a Wednesday afternoon when something jumps out: Kalshi has a Fed rate-cut contract trading at 48 cents, while another platform is showing 53 cents for what looks like the exact same thing. Buy the yes on Kalshi at 48 cents and the no on the other platform for 47 cents, and you're guaranteed to win money in theory.

It feels like free money, but what looks like easy arbitrage is usually more complicated. Here are some things to check before you start bragging to the group chat.

Step 1: Are These Really the Same Contract?

On the surface, both contracts ask the same question: Will the Fed cut rates in 2025?

But look closer. Kalshi might phrase it as: "Will the Fed cut rates by December 31, 2025?" Another platform could phrase it as: "Will the Fed cut rates at or before the Fed's December 2025 meeting?" Those sound similar — but they're not identical.

Imagine the Fed calls an emergency session on November 29, 2025. A cut there would trigger YES on the calendar-based contract (ends Dec 31) but NO on the meeting-based one. Suddenly your "risk-free" spread is exposed to a very real difference in settlement.

Step 2: Counting the Invisible Costs

Even if the contracts are the same, that 5¢ spread shrinks once you account for fees, bid-ask spreads, and the friction of moving money between venues. What looks like five points on the screen might net out to two — or worse, zero — once the dust settles.

Step 3: The Fill Problem

Let's say you grab the Kalshi YES at 48. Before you can buy the NO bet on the other platform at 47, the price might jump to 49. Now your profits have dropped significantly.

In general, just remember to do your due diligence — free lunches via arbitrage are hard to come by. If you want a step-by-step walkthrough of the basic math, see our guide on how to check for arbitrage.

Build with this data

Automate your strategies, create arb bots, or build your own dashboard. Free tier includes 1,000 requests/mo across all prediction market platforms.

Free Trading Tools

View allCompare fees across Kalshi, Polymarket & PredictIt.

Find fair probabilities with the overround removed.

See if a trade has positive EV before you enter.

Convert American, decimal & implied probability.

Combined odds and payouts for multi-leg bets.

Your real take-home after fees and taxes.

Related Posts

How to Build a Prediction Market Trading Bot: A Practical API Guide

A technical walkthrough of the APIs, SDKs, strategies, and hard-earned lessons behind building automated trading systems for prediction markets — from your first API call to a working bot.

11 min readRead

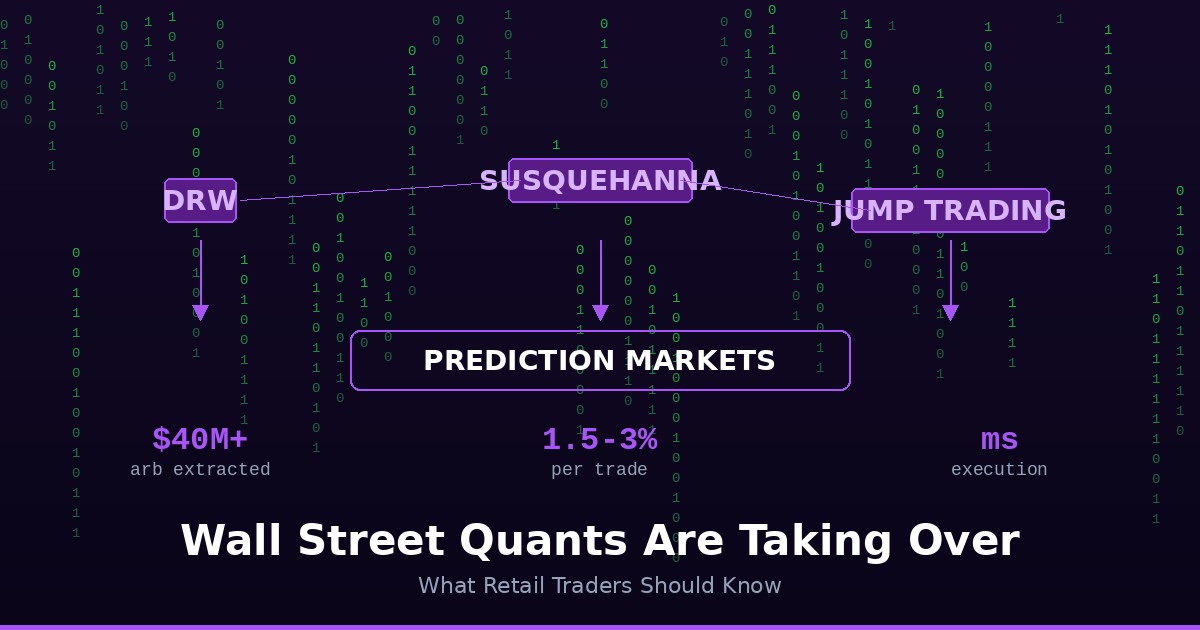

Wall Street Quants Are Taking Over Prediction Markets: What Retail Traders Should Know

DRW, Susquehanna, and Jump Trading are building dedicated prediction market desks. Here's how institutional money changes the game — and where retail traders still have an edge.

7 min readRead

Position Sizing in Prediction Markets: The Kelly Criterion Guide

The Kelly Criterion, fractional Kelly, correlation risk, and why most prediction market traders blow up not because they're wrong — but because they bet too much when they're right.

13 min readRead