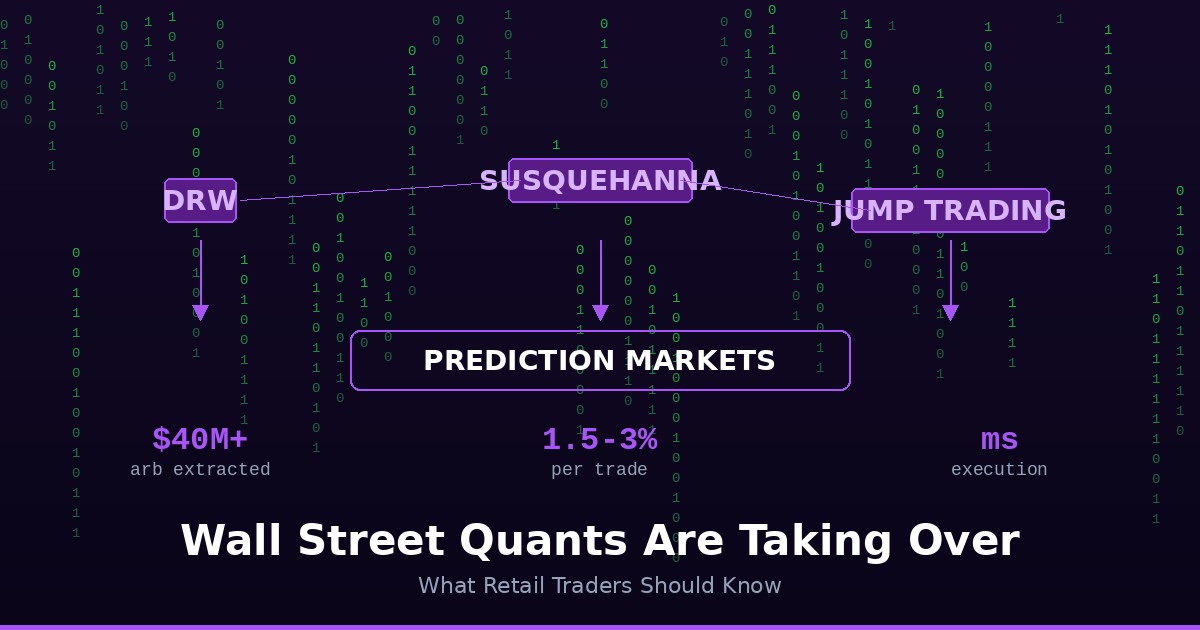

Wall Street Quants Are Taking Over Prediction Markets: What Retail Traders Should Know

DRW, Susquehanna, and Jump Trading are building dedicated prediction market desks. Here's how institutional money changes the game — and where retail traders still have an edge.

TL;DR: Wall Street quant firms like DRW, Susquehanna, and Jump Trading have built dedicated prediction market trading operations. Manual arbitrage on major markets is effectively dead. But retail traders with real domain knowledge still have edges in niche markets that algorithms can't easily model.

Something shifted in prediction markets over the past year that most retail traders haven't fully processed: the quants showed up.

DRW, Susquehanna International Group, and Jump Trading — proprietary trading firms that collectively deploy tens of billions in capital across traditional financial markets — have each built dedicated prediction market trading operations. These aren't exploratory projects or one-off trades. These are staffed desks with quantitative researchers, engineers, and execution infrastructure purpose-built for event contract markets.

(Source: Finance Magnates, DL News)

The implications for retail traders are significant. Not catastrophic — but significant. Understanding what changed, and where the edge has moved, is the difference between adapting and getting arbitraged out of the market.

What the Quants Are Actually Doing

Quantitative trading firms approach prediction markets the same way they approach any other market: with speed, scale, and systematic execution.

Cross-platform arbitrage is the most visible strategy. When the same event trades at 52¢ on Kalshi and 56¢ on Polymarket, a quant firm's bot will spot the discrepancy, calculate the net profit after fees, and execute both sides of the trade in milliseconds. Between April 2024 and April 2025, over $40 million in arbitrage profits were extracted from Polymarket alone, with automated systems capturing the vast majority. (Source: Yahoo Finance / DL News analysis)

These aren't the 5-cent spreads that a human trader might spot on a Wednesday afternoon. They're 1.5 to 3 cent edges executed thousands of times across hundreds of markets simultaneously. Individually small. Collectively enormous.

Market making is the less visible but equally important strategy. Quant firms provide continuous bid-ask quotes across markets, earning the spread on every trade that passes through their orders. This is the same role they play on stock exchanges and options markets — and in prediction markets, where natural liquidity is thinner, the margins for market makers are better.

Statistical modeling is where it gets interesting. These firms apply the same quantitative techniques used in sports betting, options pricing, and macro trading: building models that price events based on historical data, correlated signals, and real-time information flow. When their model says a contract is worth 61¢ and it's trading at 57¢, they buy. When it overshoots to 65¢, they sell. Rinse, repeat, at scale.

What This Means for the Markets

The presence of institutional traders fundamentally changes market structure:

Prices Got More Efficient

Markets that used to sit at obviously wrong prices for hours — a contract trading at 30¢ when anyone following the news could see it should be 45¢ — now correct in minutes or seconds. Institutional arbitrage compresses pricing gaps and forces prices closer to true probabilities. For the market as a whole, this is good. For a retail trader who relied on lazy pricing, the free lunch is over.

Spreads Got Tighter

Market makers quoting on both sides of a contract compress the bid-ask spread. Where a thinly traded market might have had a 5-8 cent spread, active market making can bring that down to 1-2 cents. This benefits every trader: when you buy, you pay less above fair value. When you sell, you get more. The cost of entering and exiting positions has dropped meaningfully.

Liquidity Got Deeper

More institutional capital means more size at each price level. If you want to buy 5,000 shares, you're less likely to move the price against yourself than you were a year ago — at least on high-volume markets. For larger retail traders, this is a genuine improvement in execution quality.

Where Retail Traders Still Have an Edge

The narrative that "quants killed retail trading" is wrong — but it requires nuance.

What's dead: manual arbitrage on major markets. If you were making money by scanning two browser tabs for price discrepancies on headline political or sports markets, that strategy is over. Bots are faster than you. They always will be.

What's alive: domain expertise in niche markets.

Quantitative models are excellent at pricing events where historical data is abundant and variables are well-defined. They struggle with:

1. Novel Events

When a market opens on a genuinely new question — a first-of-its-kind geopolitical scenario, a regulatory decision with no precedent, a tech milestone with unclear timeline — models have limited historical data to train on. A human who deeply understands the domain can form a more accurate probability estimate than an algorithm working from sparse data.

2. Local and Niche Knowledge

A quant desk in Chicago isn't going to know more about a niche entertainment market, an obscure political primary, or a specific sports prop than someone who follows that domain obsessively. The less mainstream the market, the less likely institutional money has built a model for it.

3. New Contract Launches

The first few hours after a new market opens are often the most inefficient. Models need time to calibrate. Liquidity providers need time to set up. If you're watching a platform and a new contract launches on a topic you understand well, you can move before the algorithms have fully priced it.

4. Resolution Rule Nuances

Every platform has different resolution criteria, and the differences matter. Quant models often treat the same question across platforms as identical. But the fine print on how a contract resolves can create real divergences that a human with platform-specific knowledge can exploit.

How to Adapt Your Strategy

If you're a retail prediction market trader, here's how to position yourself in the institutional era:

Specialize. Pick 2-3 domains you genuinely know well — not markets you trade because they're popular, but areas where you have a real informational or analytical advantage. Go deep, not wide.

Trade thinner markets. The institutional edge is concentrated in the most liquid, most watched markets. Move to where they're not. Less volume means wider spreads, but it also means more pricing inefficiency for an informed trader to capture.

Use cross-platform tools. Even if manual arbitrage on individual contracts is dead, structural price differences across platforms still exist — driven by different user bases, different fee structures, and different liquidity profiles. Prediction Hunt shows you every major market's price across platforms in real time so you can find where you're getting the best deal.

Think longer-term. Quant strategies are typically optimized for short-term edge capture — buy, sell, move on. If you have a genuine thesis about how an event will unfold over weeks or months, you can take a position at today's price and hold through the noise that algorithms are trading around.

Size appropriately. If you're trading in an environment with professional counterparties, position sizing matters more than ever. Overbetting your edge is the fastest way to give back whatever advantage your domain knowledge provides.

The Bottom Line

Wall Street's arrival in prediction markets is a structural change, not a temporary phase. The days of easy arbitrage and obviously mispriced contracts in major markets are over. But prediction markets are not equity markets. They resolve based on real-world events, and models can only price what they can measure.

The edge has moved. It used to be "find the mispriced contract." Now it's "know something the model doesn't." That's a harder game — but for traders who actually have domain expertise, it's a better one.

Frequently Asked Questions

Which Wall Street firms are trading prediction markets?

DRW, Susquehanna International Group, and Jump Trading have all built dedicated prediction market trading operations as of 2026. These proprietary trading firms bring quantitative modeling, automated execution, and market-making infrastructure that mirrors their operations in traditional financial markets.

Can retail traders still make money in prediction markets?

Yes. Institutional traders dominate high-volume, efficient markets with automated strategies. But prediction markets cover thousands of contracts across politics, sports, entertainment, economics, and more. Retail traders with genuine domain expertise can find edges in niche markets, new contract launches, and categories where algorithms have limited training data. The strategy shift is from "find obvious mispricings" to "know more than the model."

Is prediction market arbitrage still possible?

Pure cross-platform arbitrage on major markets is effectively captured by bots that execute in milliseconds. Over $40 million in arbitrage was extracted from Polymarket alone between April 2024 and April 2025. However, structural inefficiencies — different fee structures, resolution rule variations, platform-specific liquidity gaps — still create opportunities for informed traders. Check Prediction Hunt to compare prices across platforms.

How much money have quant firms made from prediction market arbitrage?

Over $40 million in arbitrage profits were extracted from Polymarket alone between April 2024 and April 2025. Automated bots executed thousands of trades capturing typical margins of 1.5-3% per trade. This figure represents only one platform and likely underestimates total cross-platform arbitrage profits industry-wide.

This article is for informational purposes only and does not constitute investment or financial advice.

Build with this data

Automate your strategies, create arb bots, or build your own dashboard. Free tier includes 1,000 requests/mo across all prediction market platforms.

Free Trading Tools

View allCompare fees across Kalshi, Polymarket & PredictIt.

Find fair probabilities with the overround removed.

See if a trade has positive EV before you enter.

Convert American, decimal & implied probability.

Combined odds and payouts for multi-leg bets.

Your real take-home after fees and taxes.

Related Posts

How to Build a Prediction Market Trading Bot: A Practical API Guide

A technical walkthrough of the APIs, SDKs, strategies, and hard-earned lessons behind building automated trading systems for prediction markets — from your first API call to a working bot.

11 min readRead

How to Evaluate Prediction Market Liquidity Before You Trade

A practical guide to checking depth, spreads, and fill quality before you commit capital. Stop getting worse prices than you expected.

9 min readRead

Why the Same Market Has Different Prices on Kalshi vs Polymarket

The same question can trade at 52¢ on one platform and 58¢ on another. It's not a glitch — it's liquidity, demographics, fees, and market structure. Here's what drives the gap.

7 min readRead